In today’s highly regulated business environment, companies that manage employee benefit plans face increasing legal exposure. Fiduciary liability insurance is designed to protect businesses and plan administrators from claims related to the mismanagement of employee benefit plans.

Whether you’re a small business owner, HR director, or corporate executive, understanding fiduciary liability coverage is critical for long-term financial protection.

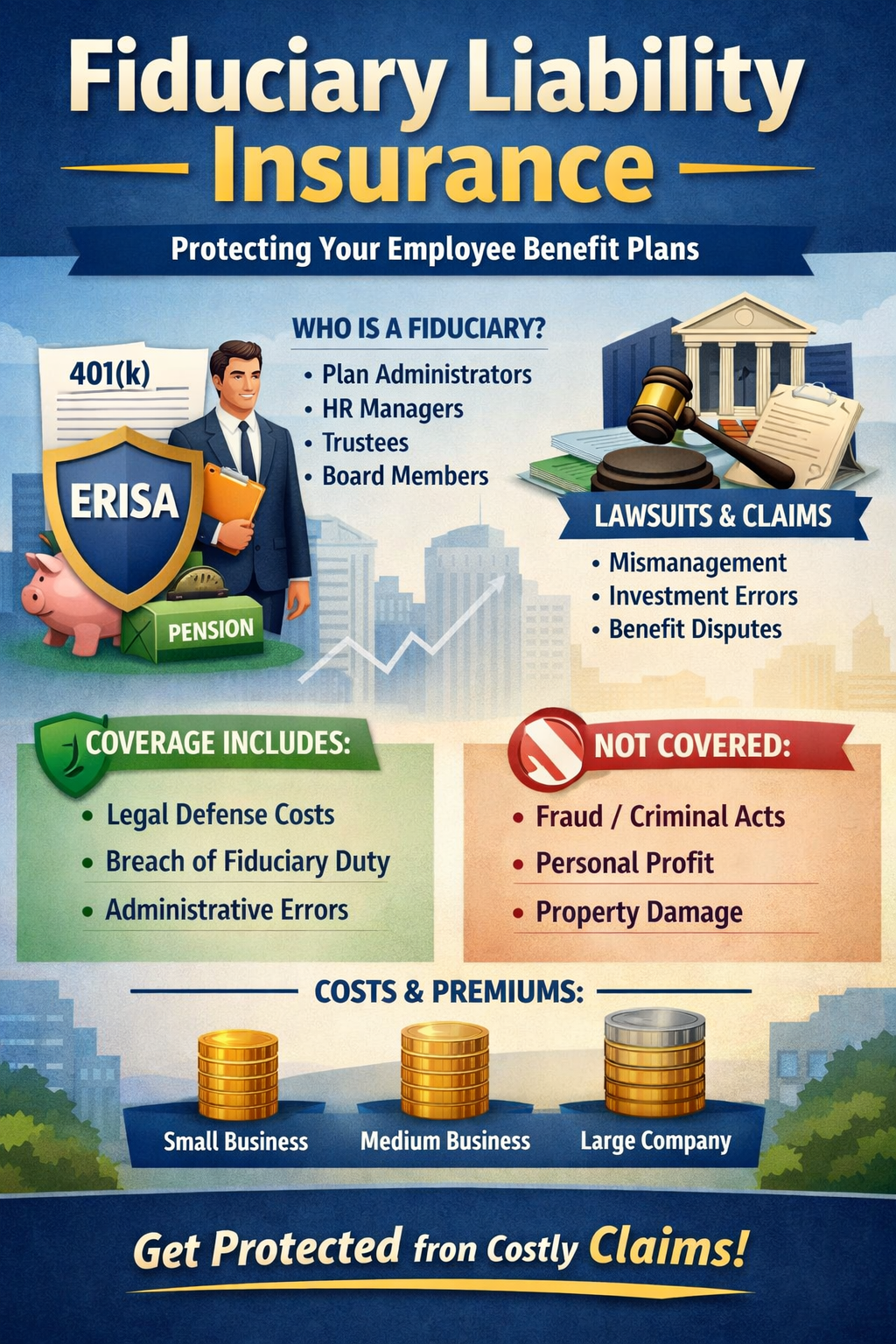

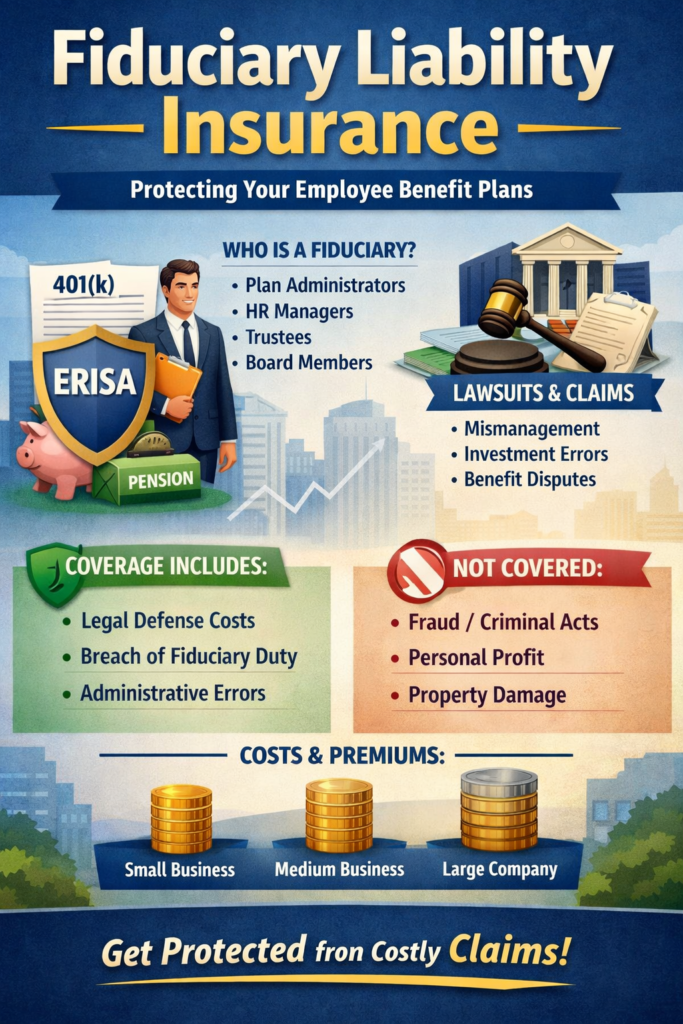

What Is Fiduciary Liability Insurance?

Fiduciary liability insurance is a specialized policy that protects organizations and individuals who manage employee benefit plans. These plans may include:

- 401(k) and retirement plans

- Pension plans

- Health and welfare benefit plans

- Employee stock ownership plans (ESOPs)

Under the Employee Retirement Income Security Act (ERISA), fiduciaries are legally required to act in the best interests of plan participants. If they fail to do so—even unintentionally—they can be held personally liable.

This insurance helps cover:

- Legal defense costs

- Settlements and judgments

- Regulatory penalties (where insurable by law)

Who Is Considered a Fiduciary?

A fiduciary is anyone who:

- Exercises discretionary control over a benefit plan

- Manages plan assets

- Provides investment advice for compensation

- Has administrative authority over plan operations

This can include:

- Business owners

- Board members

- HR managers

- Plan trustees

- Investment committee members

Even routine administrative mistakes can trigger expensive lawsuits.

Why Fiduciary Liability Insurance Is Important

1. Personal Liability Risk

Under ERISA regulations, fiduciaries can be held personally responsible for financial losses to a benefit plan.

2. Rising Litigation

Employee benefit plan lawsuits have increased significantly in recent years, especially involving excessive fees and mismanagement of retirement plans.

3. Regulatory Investigations

Government agencies may investigate plan practices. Legal defense costs alone can be substantial—even if the claim has no merit.

4. Gaps in Other Policies

Many business owners assume their General Liability or Directors & Officers (D&O) covers fiduciary claims. In most cases, it does not.

What Does Fiduciary Liability Insurance Cover?

A comprehensive fiduciary liability insurance policy typically covers:

✔ Breach of Fiduciary Duty

Claims alleging negligence, errors, or omissions in plan management.

✔ Mismanagement of Investments

Failure to properly monitor or diversify plan investments.

✔ Administrative Errors

Enrollment mistakes, incorrect benefit calculations, or failure to update plan documents.

✔ Failure to Follow Plan Documents

Non-compliance with established procedures.

✔ Defense Costs

Attorney fees, court expenses, and settlement payments.

What Is Not Covered?

Understanding exclusions is equally important. Common exclusions include:

- Criminal or fraudulent acts

- Personal profit gained illegally

- Bodily injury or property damage claims

- Intentional wrongdoing

Always review policy terms carefully with an insurance advisor.

How Much Does Fiduciary Liability Insurance Cost?

The cost of fiduciary liability insurance depends on several factors:

- Company size

- Number of employees

- Plan assets under management

- Claims history

- Industry risk level

Estimated Annual Premiums:

- Small businesses: $500 – $2,500

- Mid-sized companies: $2,500 – $10,000+

- Large corporations: Higher depending on asset size and exposure

While premiums vary, the cost is minimal compared to potential legal settlements.

Fiduciary Liability Insurance vs. ERISA Bond

Many business owners confuse fiduciary insurance with an ERISA bond.

ERISA Bond

- Required by law for most plans

- Protects the plan from theft or fraud

Fiduciary Liability Insurance

- Optional but strongly recommended

- Protects fiduciaries from lawsuits related to plan management

Both serve different but complementary purposes.

Who Needs Fiduciary Liability Insurance?

You should consider fiduciary liability coverage if your business:

- Offers a 401(k) plan

- Manages pension funds

- Administers health benefit programs

- Has a retirement investment committee

- Handles employee stock ownership plans

Even small companies face regulatory exposure.

Real-World Claim Examples

To understand the importance of fiduciary liability insurance, consider these common scenarios:

- A company fails to monitor high-fee investment options in a 401(k) plan, leading to participant lawsuits.

- An HR department makes administrative errors causing employees to lose coverage.

- A fiduciary is accused of not diversifying plan investments properly.

In each case, defense costs alone could exceed six figures.

How to Choose the Right Policy

When shopping for fiduciary liability insurance, evaluate:

1. Coverage Limits

Ensure limits match your plan asset size and risk profile.

2. Retroactive Date

Check how far back prior acts are covered.

3. Defense Provisions

Determine whether defense costs reduce policy limits.

4. Carrier Reputation

Choose insurers with strong financial ratings and experience in employee benefits risk.

Risk Management Best Practices

Insurance is only part of the solution. Businesses should also:

- Regularly review investment options

- Document fiduciary decisions

- Conduct compliance audits

- Provide fiduciary training

- Work with experienced legal and financial advisors

Proactive governance reduces both risk and premium costs.

Frequently Asked Questions (FAQs)

Is fiduciary liability insurance legally required?

No, but ERISA bonds are required. Fiduciary insurance is optional yet highly recommended.

Does D&O insurance cover fiduciary claims?

Typically no. Most D&O policies exclude ERISA-related claims.

Can individuals be sued personally?

Yes. ERISA allows personal liability for fiduciaries.

How much coverage do I need?

Coverage should reflect plan asset size and potential litigation exposure.

Final Thoughts

Fiduciary liability insurance is no longer optional for businesses that manage employee benefit plans—it’s a critical layer of financial protection. With increasing regulatory scrutiny and growing employee awareness, even minor administrative mistakes can escalate into costly lawsuits.

By investing in the right policy and implementing strong governance practices, organizations can safeguard both corporate and personal assets.

If your business offers employee benefits, now is the time to evaluate your fiduciary risk exposure and secure proper coverage.